When you think of today’s business banks, you may not think of how far banking systems have come since their origins. But currency has been a part of our society since before banks were even invented. And the history of banking is marveled with exciting twists and turns.

From historic grain banks to the modern neobanking systems, credit cards and mobile apps we see today, a lot has changed in that time. Now, we know just how important financial institutions are to our everyday lives.

Webinar: Turn Your Business Into a Money-Making Machine

Unlock the secrets to transforming your business from a job into a profitable, cash-generating machine.

Register Now

Today, banking is undergoing a massive change as digital banking transforms how people do business. Let’s look at the evolution of banking to understand just how far we’ve come and how recent changes to our economic climate have affected banking.

In this article:

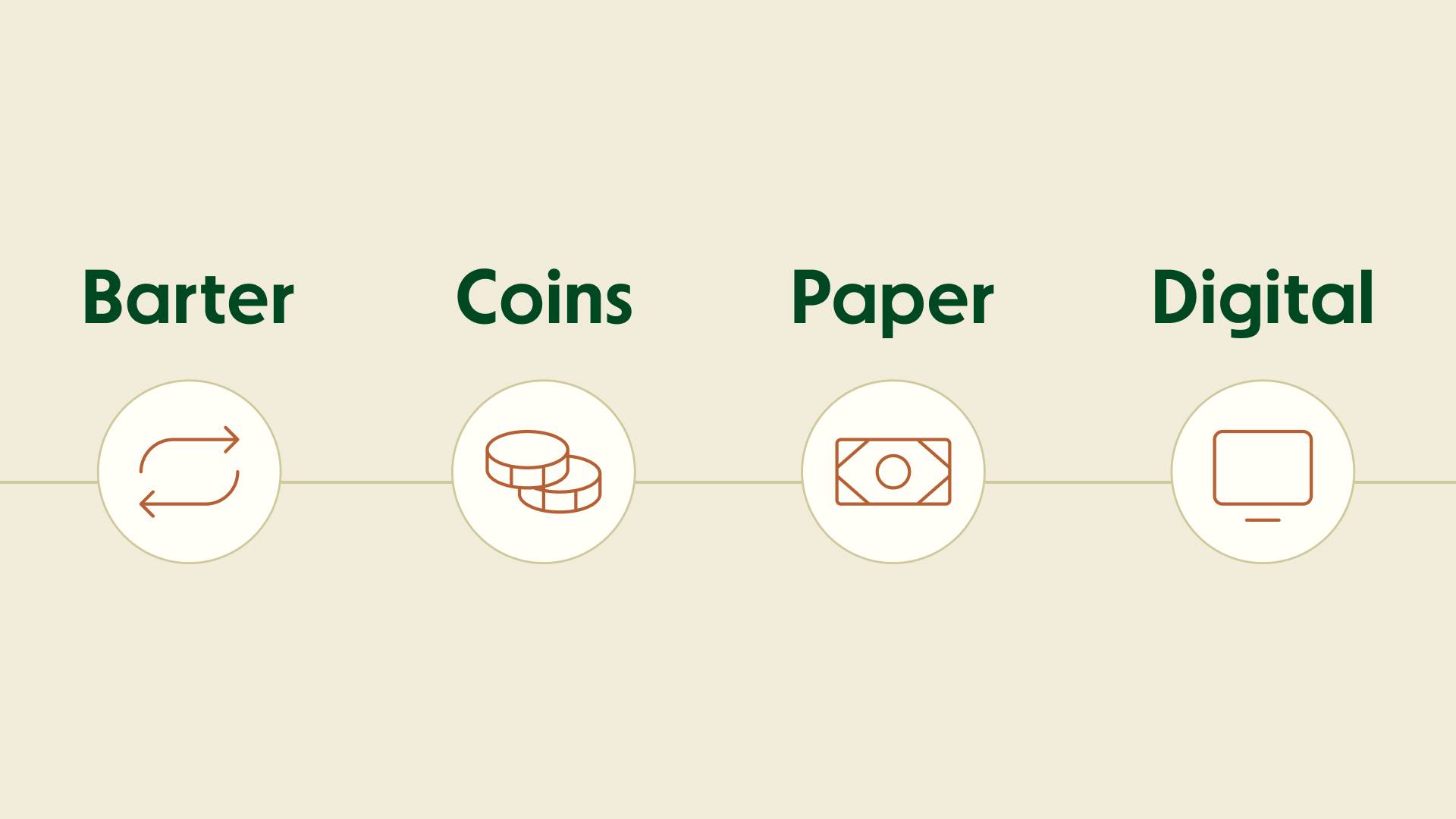

The ancient marketplace (2000 BCE)

The first bank was born around 2000 BCE in the ancient empires of Egypt, Assyria, India and Sumeria, with the exchanging of goods. The ancient marketplace used various purchasing methods, including grain banks, barter systems and metal weights to measure value.

Grain banks: Grain banks allowed harvesters to deposit grain in bulk. Then, depositors would withdraw a particular amount of grain when they wanted to make a purchase.

Barter system: The barter system paved the way for exchanging goods, but the ancient Egyptians used a more complex system. In some major cities, people gathered in public marketplaces to trade goods, similar to a public market you might see today.

Metal weights: Before using coins around 500 BCE, ancient Egyptians used a system of metal weights to measure value. Each good was weighed, and a value was assigned.

The use of metal coins (500 BCE)

As banking progressed, so did the materials used. Precious metals, like silver, bronze and gold, were already being traded, so metal coins were the natural advancement. Metal coins were used as currency for centuries after.

During the Roman Empire, banking began shifting to private depositories or safes. However, most ancient homes did not have steel safes. This meant only the wealthy could store their coins safely in the basements of temples.

It wasn’t until the 10th century that paper money was introduced during the Tang Dynasty in China. Inspired by his Silk Road travels and this unique Chinese method, Marco Polo introduced the idea of paper money to Europe, and banking became more widely used. Having a standard currency made tax collection easier, so countries had a strong incentive to standardize. Paper currency was also far less expensive to maintain than metal coins.

Free-market banking (1759)

British economist Adam Smith introduced the “invisible hand” theory in 1759. This theory characterized the mechanisms through which beneficial social and economic outcomes may arise from the accumulated self-interested actions of individuals.

More simply put, the invisible hand theory helped spark the idea that banking should exist without government intervention. This free-market banking concept first started being put to use in the United States of America as the country was emerging.

Empowered by these views of a free-market economy, U.S. bankers limited the state’s involvement in the banking sector. However, after the Revolutionary War, Secretary of the Treasury, Alexander Hamilton, created the first central bank in the U.S. and a national currency was born.

The Federal Reserve (1913)

In 1913, the U.S. government formed the Federal Reserve Bank (the Fed) to monitor and oversee banking activity. Even so, financial power was concentrated on Wall Street. When World War I broke out, the United States became a global lender and the center of the financial world.

The Federal Reserve system began requiring all debtor nations to pay back their war loans before any American institution would extend them further credit. So when the stock market crashed during the Great Depression in 1929, brokers called in bank loans that could not be paid back. Banks began to fail as debtors defaulted and depositors attempted to withdraw their deposits. This led to around 9,000 bank failures in total.

In response, new banking regulations and regulatory agencies emerged to restore the merchant banking sector and repair people’s confidence in the system. The Federal Deposit Insurance Corporation (FDIC) was created to better insure accounts and instill this confidence. Later, in 1944, the World Bank was established to rebuild the economies of postwar Europe.

Webinar: Turn Your Business Into a Money-Making Machine

Unlock the secrets to transforming your business from a job into a profitable, cash-generating machine.

Register NowModern banking (1960)

World War II saved the banking industry because the war required financial decisions concerning billions of dollars. This massive financing operation created companies with huge credit needs that prompted banks to merge. These massive banks spanned global markets.

Because of this, domestic banking in the United States was more prevalent and lending became available to the average citizen. This gave way to the modern banking system we know today, including deposit insurance and widespread mortgage lending.

Since the revolutionary invention of ATMs in 1967, banking technology has flourished. Now, banking is accessible to all Americans with new technology emerging every day.

The rise of neobanks (late 20th century)

Although banks have gone through many major developments throughout the decades, the introduction of digital banks in the late 20th and early 21st centuries is one of the most significant. Today, people need more than just a place to store their money. Since their advent, neobanks have transformed to offer the most powerful digital solutions for banking.

Unlike traditional banking systems, neobanks offer mobile banking features that allow business owners to manage their finances wherever they are. Visiting commercial bank branches is now a thing of the past. Instead, online banks allow you to see your cash flow like never before, from anywhere in the world and at any time.

With neobanks continuing to expand their digital services, there’s no telling what the future of online banking will look like. Now, business owners can make quick financial decisions without the limitations of traditional banking.

Understand the differences between digital banking vs. traditional banking

The future of banking

While the future of banking services looks bright, the current financial climate will no doubt change the way we manage money — especially for small business owners and startups. Since the pandemic began, businesses have struggled to deal with the rising costs of hyperinflation and the change in interest rates, increasing the need for digital banking solutions.

During this time of economic uncertainty, evolving banking expectations and technological advances are paving the way to a complete transformation of the banking ecosystem. As it stands, it’s unclear exactly what the future holds for banking infrastructure.

Webinar: Turn Your Business Into a Money-Making Machine

Unlock the secrets to transforming your business from a job into a profitable, cash-generating machine.

Register NowWhat we do know is that digital banking will continue to dominate financial institutions, likely progressing advancements like artificial intelligence (AI) and application programming interface (API) software. For business owners, this means better technology to help you make intelligent financial decisions for your business.

Managing your finances with Relay

Here at Relay, we’re helping shape what the future of banking looks like. Relay’s online business banking and money management platform helps small businesses get clarity into their spending and control of their cash.

Relay goes beyond the everyday banking basics with:

✅No account fees, overdraft fees or minimum balances

✅Up to 20 individual checking accounts

✅50 virtual or physical Mastercard® debit cards

✅Payments and deposits via ACH, wire and check

✅Deposits from payment processing providers like PayPal, Stripe and Square

✅Direct integrations with accounting software like QuickBooks Online and Xero

If you’re looking for an online banking solution that puts you in control of your cash flow, check out Relay—you can sign up here!