Brex and Divvy are both financial technology companies that offer expense management tools and credit card services to small-to-medium-sized businesses.

Brex is an FDIC-insured bank, offering bank accounts to small businesses, while Divvy specializes in business credit cards, bill pay, and expense management software. Notably, Divvy is not a banking provider.

Recently, Brex announced they would only serve funded startups and larger SMBs, even to the point of removing users who don’t fit into that profile from the company’s services.

Is Divvy a solid Brex alternative? Here’s our thorough review comparing both fintech solutions.

IN THIS ARTICLE

🏦 What is Brex?

Brex is a modern business banking solution offering bank accounts, corporate cards (both physical and virtual cards), expense management and other tools for funded startups and enterprise companies.

Companies that find themselves with venture-backed cash need comprehensive spend controls to ensure that investor dollars are driving growth. With Brex, you can issue physical and virtual charge cards, give employees access to real-time expense reporting, and seamlessly integrate banking with accounting software and payment processors like Stripe.

The level of banking Brex provides is comprehensive, which is why they've recently shifted upstream to service enterprise companies and venture-backed startups who require this kind of complex workflow.

💳 What is Divvy?

Divvy is an “all-in-one spend management solution" with a big emphasis on the management of funds and expense tracking. The platform has a wide variety of tools to help increase visibility on expense management and help business owners make important financial decisions.

While they do not offer business bank accounts, you are able to connect an existing business bank account to Divvy to make payments and move cash.

Divvy has solutions for both small and medium-sized SMBs, with the potential for larger organizations to benefit from their platform, too.

⚖️ Brex vs. Divvy: What's the difference?

The main difference between Brex and Divvy is that Brex is a digital-only banking and spend management platform that serves venture-backed tech startups, whereas Divvy is an expense management, spend tracking and corporate credit card platform that serves small businesses.

📋 Brex vs. Divvy comparison chart

Here's a detailed chart that compares the main differences and similarities between Brex and Divvy:

Feature | Brex | Divvy |

|---|---|---|

Businesses of any size can open an account | ❌ | ✅ |

Type of businesses served | Enterprise companies | SMBs with 1 - 500 employees |

No monthly account fees | ✅ | ✅ |

No minimum balance requirements | ✅ | ✅ |

No overdraft fees | ✅ | ✅ |

Free ACH payments | ✅ | ✅ |

Free check payments | ✅ | ✅ |

No fees on deposits | ✅ | ✅ |

Domestic wires | Free | Coming Soon |

International wires | Free | Coming Soon |

Same-day ACH | ❌ | ❌ |

Free checking accounts | 8 | ❌ |

Savings accounts | ❌ | ❌ |

Debit cards | ❌ | ❌ |

Credit cards | ✅ | ✅ |

Cashback and rewards on card spend | ✅ | ✅ |

Accounts payable automation | ❌ | Available through Bill.com |

Request payee information | ❌ | ✅ |

QuickBooks Online integration | ✅ | ✅ |

Xero integration | ✅ | ✅ |

Gusto integration | ✅ | ✅ |

Trustpilot rating | 3.7 (Source) | 2.9 (Source) |

Are you looking for a business bank for your small business? Try Relay — we're rated 4.5 on Trustpilot! Here's how Brex vs Relay compare.

🔐 Qualifying for an account

Divvy has two main offerings. One is for businesses that have 1 to 20 employees and another one for businesses up to 500 employees — covering the whole spectrum of the SMB landscape.

However, when it comes to their requirements for qualifying for an account, potential clients must go through the process of requesting a demo. Once that is done, an account representative makes contact to continue the onboarding process.

Their terms and conditions page doesn’t go into specifics other than being eligible to sign a contract in the US and being a recognizable business entity.

Brex has a similar process when it comes to onboarding new customers. You have to get in touch with their client onboarding team who will then guide you through the rest of the process to determine business eligiblility. Brex does note on their website that they do want to see at least $25,000 in your account balances, in addition to the upmarket clientele they now serve.

In terms of pricing, both Brex and Divvy are free to use, with no subscriptions or annual fees involved. Divvy gets a share of merchant transaction fees, which is how they make money. Brex earns money through referral fees in their perks program and partnerships, earning interest on cash of account and cardholders, and merchant fee sharing (similar to Divvy).

Neither Divvy nor Brex requires a personal credit check, credit score, or personal guarantee. However, Brex scrutinizes cash flow, spending habits, and funding levels for each new client. Divvy makes strides to help SMBs build their company credit, with their “Credit Builder” program with secured cards available. These cards have credit limits similar to the amount in a designated account.

🤝 Banking collaboration with accountants

Brex and Divvy both have integrations with Quickbooks Online and other accounting software.

Both platforms offer several options when it comes to user management. However, both companies attempt to keep users on their respective platforms by providing most of the tools necessary.

Divvy puts a big emphasis on its ability to have customizable spending limits on employee cards and has other complementary tools to help enforce budgets and gain natural time intelligence.

💰 Cashback and rewards

Brex and Divvy take similar approaches when it comes to their cashback and rewards programs.

Both platforms have a points system where you can accumulate points over a given period and trade them in for discounts or other promotions. Additionally, they both offer a series of discounts from popular vendors such as Amazon Web Services, major hotel chains, restaurants and car rental companies.

In this regard, it seems that you would be getting something very similar from both of these SMB expense management solutions.

🔁 Accounts payable management

The two companies have different approaches when it comes to accounts payable maangement.

Divvy’s accounts payable management is handled by Bill.com, their parent company, which is a full-fledged account payable management software. You get customizable automation functions as well as seamless integration with your accounting tech stack. However, the pricing aspect is not clear since Bill.com has a different pricing structure than Divvy, so you may have to pay additional fees.

Brex does not have accounts payable automation, but rather focuses on streamlining expense management for team members at larger organizations. Businesses can create expense policies for employees, send unpaid invoices to Brex via email, and employees can request the ability to make purchases, increase limits on cards or issue vendor-specific cards. Plus, they're developing new spend management tools that are currently being tested.

🆚 Verdict: Which expense management alternative is right for you?

If you’re a small business with 1 to 100 employees, have a bank account you like, and you’re looking to build your company’s credit score — Divvy is the clear winner between the two.

On the other hand, if you have VC executives who want detailed reports and a comprehensive financial tracking system (and you meet the requirements) Brex could be the right option.

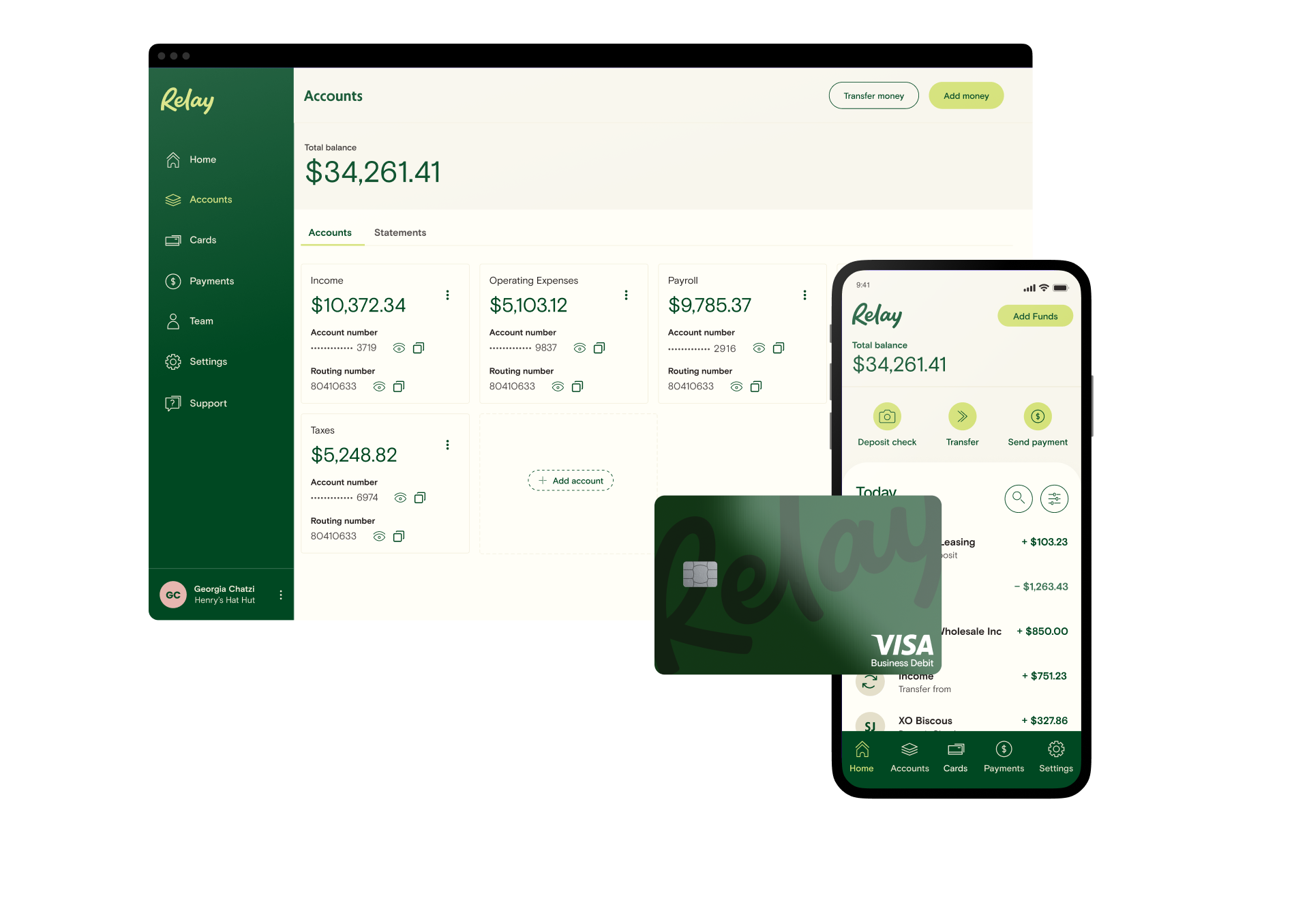

And if you're neither? Then consider an online banking and money management platform like Relay.

📊 Cash flow management with Relay

As many as 60% of all small businesses report having a cash flow issue at some point in their company’s history. Relay solves this by providing an online banking and money management platform to help small businesses understand precisely what they're earning, spending and saving.

Whether you're looking for common sense spend controls or the ability to create virtual cards that allow you to free up some decision-making to your small team, Relay helps your business get crystal clear on your cash flow.

We’re a digital-first banking platform offering small businesses easy, yet powerful expense management, spend controls, employee cards, and multiple bank accounts — for free. Relay is FDIC insured via Thread Bank. Take a closer look at Relay.